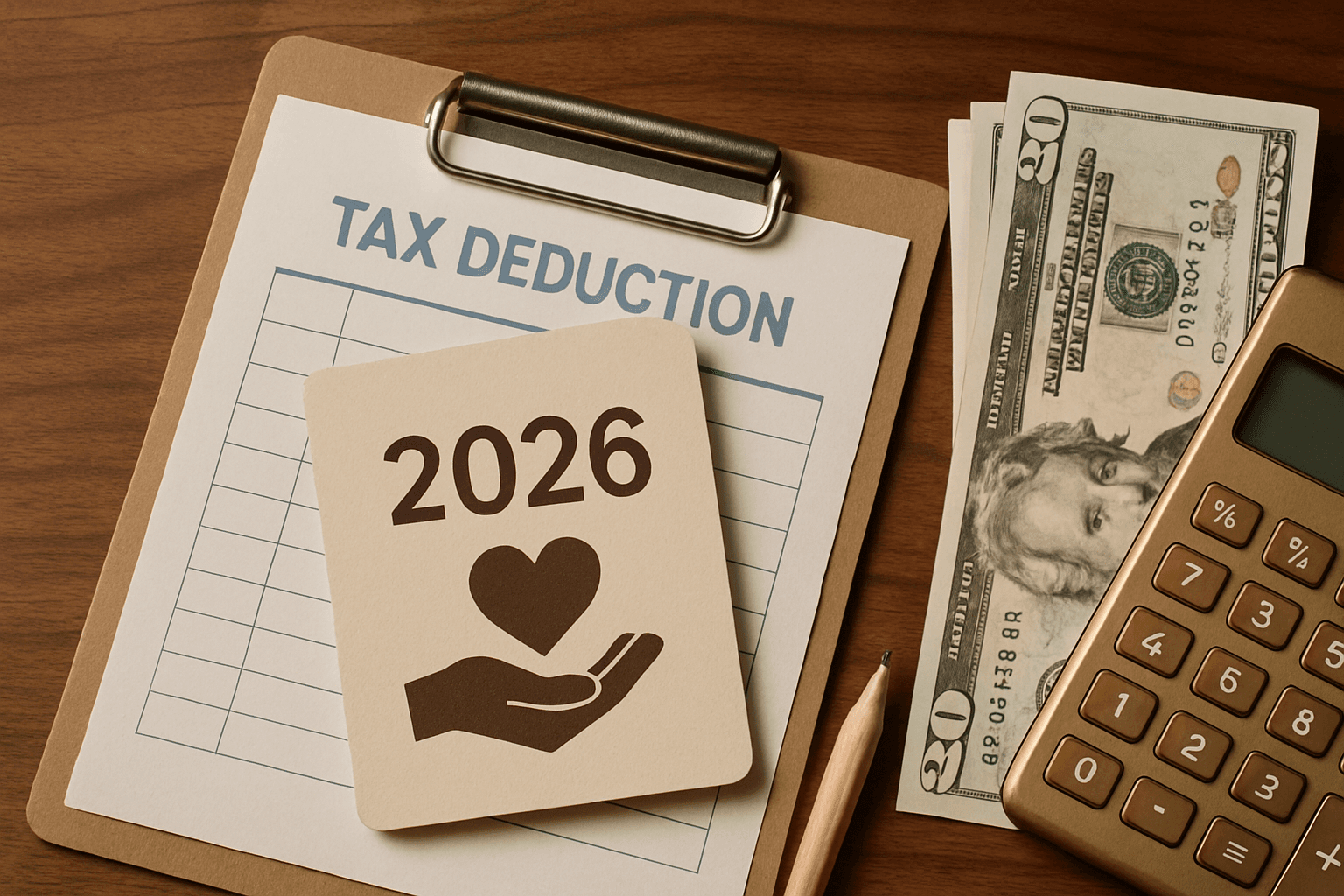

Charitable Giving in 2026: Don’t Miss the Deduction if You Take the Standard Deduction

Starting in 2026, many taxpayers who use the standard deduction can still claim a separate deduction for qualifying cash gifts. The right result depends on your filing status, gift type, records, and whether itemizing actually beats the standard deduction.

Kwon CPA

Many owners give regularly—to a church, a school, a local food program, or a neighborhood fundraiser. That generosity may be personal, tied to the business, or a mix of both. For tax purposes, though, the details matter: who made the gift, where it went, what was donated, and what proof you kept.

The charitable deduction rules change in 2026. The biggest practical change helps people who do not itemize. But it does not mean every gift is deductible, or that you can simply add every receipt to your return. Before making year-end gifts, compare the two deduction paths using your own numbers.

1. Start with the real decision: standard deduction or itemizing

Every individual return generally takes one of two routes. You either claim the fixed standard deduction or itemize qualifying expenses such as mortgage interest, state and local taxes (SALT), charitable gifts, and certain medical expenses. You do not get both; the useful choice is usually the larger deduction.

For 2026, the standard deduction is $16,100 for a single filer and $32,200 for a married couple filing jointly. Think of that number as the line your itemized deductions need to clear. A couple expecting $18,000 of mortgage interest, $9,000 of property and state income taxes, and $4,000 of qualifying charitable gifts should calculate their itemized result before assuming it will win.

Also separate business giving from personal giving. If your restaurant corporation sponsors a local event, its treatment may differ from a personal donation reported on Schedule A. A payment made for advertising or promotion is not analyzed the same way as a pure charitable gift. Keep business-card charges and personal-card gifts in separate records from day one.

The tax value of a gift depends less on how much you gave than on which deduction path actually fits your return.

2. The new cash-gift deduction for standard-deduction filers

Starting in 2026, taxpayers who take the standard deduction may still claim a separate deduction for qualifying cash contributions. The limit is up to $1,000 for a single filer and up to $2,000 for a married couple filing jointly. This gives many households a reason to track direct cash gifts even when their itemized deductions fall below the standard-deduction amount.

Three boundaries matter. First, this is for cash contributions. Checks, card payments, and bank transfers are easier to document and manage than loose cash. Clothing, furniture, inventory, vehicles, and stock do not qualify for this separate deduction. Second, the money must go directly to an eligible organization. Helping a relative with rent or sending money to a neighbor’s personal fundraiser may be generous, but it is not a deductible charitable contribution. Third, if you itemize, you cannot stack this extra $1,000 or $2,000 on top of your Schedule A charitable deduction. Itemizers calculate their gifts on Schedule A.

Cash dropped into a collection basket can be difficult to support without a year-end statement from the organization. Use a check, card, official online portal, or numbered envelope system that produces a record.

3. If you itemize, include the new 0.5% charitable floor

For itemizers, 2026 adds a new calculation step: the first 0.5% of your adjusted gross income (AGI) in charitable gifts does not count toward your itemized deduction. If your AGI is $150,000 and you make $5,000 in qualifying gifts, subtract $750 ($150,000 × 0.5%). Your charitable amount for this calculation is $4,250.

That change means a familiar assumption can produce the wrong answer. Consider a married couple with $10,000 of SALT, $20,000 of mortgage interest, and $5,000 of qualifying gifts. If medical expenses do not clear their separate AGI threshold, the charitable floor leaves them with $34,250 of itemized deductions. The alternative—$32,200 standard deduction plus a $2,000 direct cash-gift deduction—is $34,200. The difference is only $50.

- Build one worksheet with projected SALT, mortgage interest, medical expenses, and charitable gifts before year-end.

- When estimating itemized gifts, subtract 0.5% of AGI before comparing against the standard deduction.

- Repeating last year’s filing choice without running the 2026 numbers

- Claiming itemized charitable gifts and the separate standard-deduction cash-gift amount for the same return

4. Consider timing, not just the annual total

If you give every year but barely exceed the standard deduction, consider whether concentrating planned gifts into one year makes sense. This is often called bunching: fund two or three years of intended giving in one year, itemize in that year, and use the standard deduction in the other years.

The key is that the giving plan and cash flow must be real. Do not make a donation you cannot afford simply to chase a deduction. If your church or favorite charity needs steady annual support, a donor-advised fund (DAF) may be worth discussing. You contribute to the DAF in the year you want to claim the itemized deduction, then recommend grants to charities over time. However, a contribution to a DAF generally does not qualify for the separate direct cash-gift deduction available to standard-deduction filers.

If you hold appreciated publicly traded stock and expect to itemize, a direct stock gift may also deserve a closer look. Selling the shares first can trigger capital-gains tax. A direct transfer to an eligible charity may allow you to avoid recognizing that built-in gain while considering a charitable deduction. Holding period, deduction limits, and the charity’s ability to accept stock all matter, so confirm the details before transferring shares.

5. Protect the deduction with records gathered at the time of the gift

A charitable deduction is not built when the return is prepared. It is built on the date you give and in the records you save. For cash, check, or card gifts, retain bank records, canceled checks, card statements, or charity communications. For any single cash or property gift of $250 or more, obtain a contemporaneous written acknowledgment from the organization. It should state the amount or describe the property and disclose whether you received goods or services in return.

If you buy a $500 charity-dinner ticket and the meal is valued at $100, the amount potentially deductible is generally $400, not $500. For noncash gifts such as clothing or furniture, keep fair-market-value support. Total noncash deductions over $500 may require Form 8283. A claimed deduction above $5,000 for one item or a group of similar items may require a qualified appraisal. Publicly traded stock has different valuation rules, but cryptocurrency may still face appraisal requirements even when it trades on an exchange.

- List planned gifts by cash, property, and stock, and confirm that each recipient is an eligible organization.

- Estimate itemized deductions, including SALT and mortgage interest, before deciding whether itemizing is worthwhile.

- If using the standard deduction, separately review the limit for direct qualifying cash gifts.

- Request acknowledgments for gifts of $250 or more and organize noncash documentation before December ends.

For busy owners, the best system is usually the simplest one: one folder for donation records, separate personal and business payments, and a quick deduction comparison before the final week of the year. Your income, home, business entity, and gift types can change the answer. For a large gift, a stock transfer, or a DAF contribution, review the numbers with your tax professional before the money moves.

Next step

How would this apply to your business?

Don't just read it. In 30 minutes we'll look at where you stand and what to clean up first.

Request a 30-minute consultation